" 'The major labels want to say the glass is half full,' says Gwen Stefani's manager Jim Guerinot. 'I think everybody's getting the message: You better get a f***ing smaller glass. The music business is a different game.' "

--Rolling Stone Magazine, January 13 2006

Most people agree that the Internet and technology changes will make it possible to replace the pipe companies – the carriers, publishers, and networks that deliver the world's information, entertainment, and communication. But that change has been predicted for years. Will it really happen? If so, when? And what business and technology infrastructure needs to be created first?

In Part One, I gave an overview of the situation. This time let's look in depth at the music industry. I'll start with a summary and then explain how I got there.

Summary: E-music changes the world in unexpected ways

--I think the biggest change happening in music distribution right now isn't piracy, it's cannibalization of CD albums by e-music singles.

--I can't believe I'm saying this, but despite all the hype, the iTunes music store is actually much more powerful than most people realize. I think it may already be too late for any competitor to stop iTunes from becoming the dominant music store in the US.

--The tipping point at which the record companies will become obsolete may arrive in about two years.

--The record companies think that variable pricing for an online single will increase their profits, but the main effect will actually be to bring the tipping point closer.

I thought this was going to be an easy post to write, but I was wrong. Every time I thought I was finished, I found major new pieces of information that forced me to go back and re-write. The situation's complicated enough that I'm still not sure I got everything right. So I'll be very interested in your comments. Before we talk about where the industry's going, we need to discuss where it is now...

The music industry today

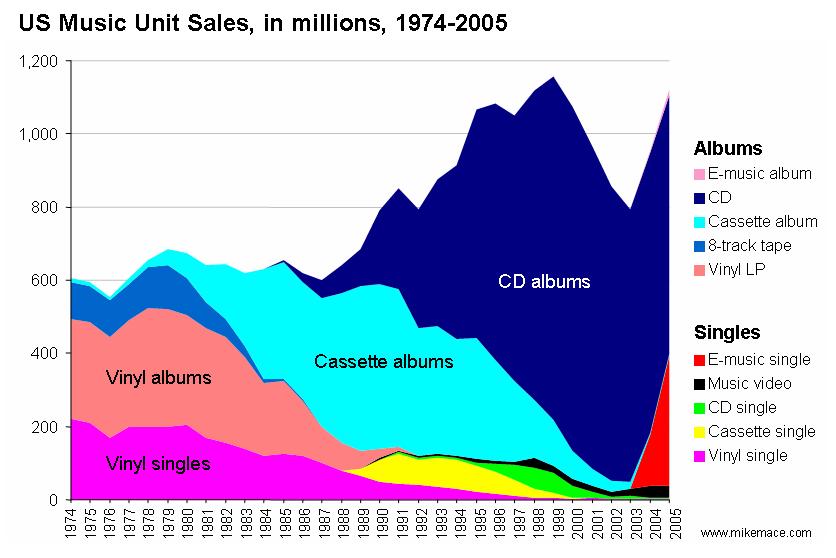

It's surprisingly hard to get clear data on what's happening in the music industry. Conditions are changing quickly, and the industry has some interesting counting practices that can easily confuse you unless you look at them very carefully. Below is the best chart I could create of music sales in the US (sorry, I couldn't find complete worldwide data). The chart shows US music unit sales by media type, from 1974 to 2005.*

Note that the chart shows unit sales, not revenue. Unit sales are a tricky thing in music – a single and an album each count as one unit. I used units because I couldn't find revenue numbers going back more than a few years. There are pluses and minuses to the units approach, which I'll discuss below.

The most striking thing you can see in the chart is the death and rebirth of the single. In 1974, singles were about a third of music unit sales, but by 2003 that share had dwindled to about 4%. That means music revenue grew much faster in the 1980s and 1990s than what you see in the chart, because customers moved from singles to more expensive albums.

Singles in a music store are a terrible buy today – a typical single on Amazon.com costs about $7-$10, and an album costs about $14. You might as well buy the album. And sure enough, most people do; about 97% of unit sales through retail are albums. The situation is reversed for e-music. On iTunes, a single costs 99 cents and an album costs about $10. Guess what, about 90% of iTunes unit sales are singles.

The big red triangle at the lower right-hand edge of the chart shows the impact of that online pricing structure. The triangle represents unit sales of e-music singles, primarily iTunes (Apple has about 70% to 83% of the US music download market, depending on which source you believe). iTunes and other online paid downloads raised the share of singles to about 25% of US unit sales in 2005, or about 353 million singles.

You can't see this in the chart, but revenue is not growing nearly as fast as units, because online singles are so much cheaper than CD albums. Rolling Stone even called 2005 the music industry's "worst ever." I guess they were thinking about musicians and record companies; music consumers had a fantastic year.

Are e-music sales still growing? A deeply pessimistic article by Bloomberg in November 2005 claimed that iTunes sales stopped growing in the summer of 2005. That drove a lot of pessimistic discussion in music industry circles, and let to a lot of criticism of Apple. If e-music has stopped growing, that would have very enormous implications for the industry, so I tried to figure out what's really happening.

Apple doesn't give clear, regular reports on iTunes music sales. It occasionally issues a press release when it hits a milestone (100m songs sold, etc), and in its quarterly financials it reports a revenue figure for the iTunes store. But that number includes revenue from sales of iPod accessories, which are pretty large. You have to find a way to remove the accessory numbers. Here's what how I did that:

In Apple's fiscal first quarter of 2006 (the three months ending December 2005), it reported iTunes revenue of $491 million. Steve Jobs said at Macworld that the company was selling three million songs a day. That would produce revenue of about $273 million. So the iTunes revenue figure that Apple reports is about 56% songs and 44% accessories.

I went to Apple's previous financial reports, extracted the iTunes revenue numbers, and applied the 56% figure to them. The resulting estimate of iTunes unit sales matched up nicely with Apple's press releases on song sales, so I'm confident that the chart you see below is roughly accurate:

As you can see, Bloomberg was spectacularly wrong -- iTunes unit sales continue to grow quickly. Why did Bloomberg get it wrong? I suspect they made the mistake of looking at quarter to quarter numbers during the summer, when consumer electronics sales almost always stagnate. Sales then explode over the Christmas period. In consumer electronics, you always have to look at year over year comparisons, not quarter to quarter.

iTunes: The Creature that Ate Motown. Setting aside the growth rate, the raw numbers themselves are pretty astounding to me. iTunes alone probably accounts for about one in every five music purchases in the United States right now, and it's continuing to grow.

I think the impact of iTunes has been understated by analysts and the press. In November of 2005, NPD issued a report saying that iTunes had jumped into the top ten US music resellers, at number seven (above Tower Records and below Circuit City). But to calculate its figures, NPD divided iTunes' unit sales by 12, to account for the fact that most iTunes sales are singles. That's appropriate if you're looking at revenue, but I think the total number of transactions is still very meaningful – it speaks to the general amount of business you're driving, and the number of people you're touching.

Think about it: if NPD had counted transactions, iTunes would have tied with Wal-Mart (20% of US music sales) as the largest music store in the United States. Considering its current growth rate, iTunes is certain to become the largest unit seller of music in the US in 2006.

People talk about iTunes as if it's an early stage business, and they discuss all the rival e-music stores as if they're all on the same level as Apple. I'm starting to think that the real question is whether iTunes has already reached a position of unassailable dominance in e-music. I don't know if anyone else in the US can develop enough momentum fast enough to overcome what Apple's doing.

There are hints that Microsoft might try, though. A recent BusinessWeek article reports that Microsoft is considering building an iPod competitor, although the hints in the article make it sound more like a PSP wannabe. Microsoft has enough financial muscle to challenge Apple, but I don't know if it has the system design skills. Maybe it knows enough, though -- all it has to do is imitate Apple, and Microsoft certainly knows how to do that...

Why did CD sales drop after 2000? There's another important point to notice in the chart. Check out the decline in total music unit sales from 2000 to 2003. This is what has the music industry so concerned about Internet piracy, which some people assume is the cause of the decline. Because albums cost more than singles, the decline actually had a larger impact on industry revenue than the chart shows. Personally, I'm sure file sharing is part of the cause. But there are a lot of other explanations as well:

--The Economist claims an internal study conducted by one of the major record companies found that only 1/3 of the drop was attributable to online piracy, with much of the blame instead going to piracy of CDs and especially to the failure of the music companies to promote interesting new music.

--A study by professors at Harvard and the University of North Carolina could find no correlation between online music downloads and reduced sales of CDs. Other studies did find a correlation. This is one of those cases where you can pick the data that matches your preconceptions.

--Some interesting charts here and here argue that the economic downturn in 2001 and rising album prices may have been at fault. The author also points out that record companies dramatically cut their new music releases in the years that sales declined. I'm not sure whether that was a cause or an effect of the sales drop, but at minimum it probably steepened the decline.

--Even some record industry execs say the decline is due in part to rising competition from other forms of entertainment, like DVDs and video games.

Whatever the cause of the album sales slowdown in the past, I think what's happening today is crystal clear: Online singles are replacing CD albums. Unless you're dying to get a full album or you're a stickler for sound quality, there's a huge financial penalty for buying music on a CD today. As that fact sinks into the minds of consumers, music downloads are almost certain to continue to grow.

Welcome to the rabbit hole, Alice

That was the straightforward part of the post. Now things get tricky. Even with the growth of e-music, the record companies are still in charge today. Most musicians are still selling through music publishers whe keep most of the revenue; the artists and record companies are just splitting a smaller pie. I wanted to calculate the tipping point, the point at which it's more profitable for a musician to sell directly through iTunes and other online stores rather than going through a record company. Bear with me while a poli sci major tries to do math...

First, let's look at the economics of music today. If you record a hit song, you'll get less than 15% of the money that people pay to buy it. Maybe you'll get less than 2%. The New York Daily News did a nice case study of what happens to the money when a group creates an album that goes gold. Their fictional rock group, Grunthead, produces a record that brings in $8.49 million. The record company and distribution channels take about 85% of that off the top, and give 15% to the group. But then there are additional charges to produce the album, plus legal and agent fees. These reduce the band members' income to just $161,909 – 1.9% of revenue.

By the way, this assumes the band wrote all its own songs. If the songs were composed by someone else, the musicians would end up roughly splitting their cut with the composer.

The economics could be very different if you sold your music directly through iTunes. Apple keeps 35% of the money paid for a song, and passes along the other 65%. Performers don't get that cut today, of course – the record company takes it. The performers generally get 10-12% of revenue, about the same as what they get from a CD sold in a store. It's fascinating to me that the artists don't get a higher percentage of e-music revenue, even though electronic distribution eliminates the whole physical distribution chain, with its production expenses, shipping costs, retail overhead, and inventory challenges. This point has been made by some very angry websites.

Anyway, if you bypass the record company you can keep the whole 65% for yourself. This makes the preliminary calculation easy – it pays to bypass the record company when e-music accounts for more than about 16% of total unit sales of music. Even though you lose a ton of CD sales, you make up the loss because you're making so much more per online sale.

But it's not that simple, because unit sales on iTunes are 90% made up of 99-cent singles, whereas in a record store they are almost all $14 albums. I don't think this is just because people go to iTunes when they want to buy singles; I think iTunes turns people into singles buyers. So the economics gets very skunky for a current musical act. If you're selling through a record company today, you get about $2.10 per album sold (15% of $14). If you switch to iTunes, and 90% of your unit sales convert to singles, you'll get an average of about $1.23 per unit that you sell (65 cents per single plus $6.50 per album). You could actually lose money per unit by going to e-music, because you trade customers down from albums to singles. Presumably you'll sell more singles because they're cheaper, and because your fans might want more than one song from your album. But I don't know how big the uplift would be, and I seriously doubt it would overcome the reduced price per unit.

In this situation, it doesn't pay to go independent until e-music accounts for more than 63% of total music unit sales. Given the rate at which iTunes is growing, that could theoretically happen by the end of the decade – but counting on exponential growth to continue for several years is one of the dumbest things you can do in high tech. So the tipping point is probably even further off.

A new hope

The easiest way to bring the tipping point substantially closer is to charge more than 99 cents for an online single. For example, if you could sell your song online for $2.99, you would make more money selling on your own as soon as e-music sales reach about 47% of total music unit sales. Considering that e-music already has 25% unit share in the US, I think 47% might be achievable in the next two to three years.

It's ironic. The record companies have been campaigning loudly for the right to charge more than 99 cents per song, so they can make more money. But if they get their way, all they'll do is facilitate their own extinction.

Be very careful what you wish for.

I'm oversimplifying

The real situation is much more complex than what I've described above. You can make yourself nuts with the permutations. For example:

The effect of price changes is unpredictable. Changing the relative prices of singles and albums will alter the sales mix in ways no one can anticipate today. That might bring the tipping point closer, or push it further away. Also, if the price of online singles goes up too much, teenagers might go back to stealing music. Then the artists and the record companies would both starve, but the lawyers would get rich.

I assumed one single would substitute for one album. If people bought two e-music singles for every CD album that gets cannibalized, the threshold for the tipping point would be years closer. Does the average album has more than one best-selling song on it/ I'll let you judge.

The whole concept of singles and albums could melt away. An interesting essay in the Guardian pointed out that the single was constrained by the amount of music you can fit on a vinyl disk rotating 45 times a minute. The three-minute format is still useful for radio and music videos, but there's no reason that a downloaded song can't be 30 seconds long or twenty minutes long. The main limitation is our own assumptions.

Also, if a music group didn't have to focus on making albums, it might be able to spend more time crafting a smaller number of truly great songs. That would improve the overall quality of popular music, even if the total number of songs being written went down.

All the more reason for Apple to allow variable pricing.

Wireless sales to mobile phones are a wild card. The record companies are starting to get significant money from ringtones. (Supposedly revenue from them was 40% of total e-music revenue last year. The unit volume would be less than 40% because ringtones often cost more than 99 cents.) It's hard for an independent artist to sell ringtones because you have to go through mobile operator contracts, something that a big record company can negotiate much more easily. This might strengthen the record companies. On the other hand, as more phones develop MP3 ringtone capability, maybe more customers will start installing their own ringtones and bypass the operators. On the other other hand, maybe the operators will disable MP3 playback in the phones they sell. Good luck mapping out what'll happen here.

All of this is analysis is US-only. The development of the music market will probably be dramatically different in other countries, where PCs (and PC-based music downloading) are less popular, and people may be more interested in downloading music directly to a mobile phone. The wireless operators certainly hope that's what'll happen. The IFPI report on music sales in 2005 says that music downloading to PCs is dominant in the US, UK and Germany, while Italy, France, and Japan are strong in downloading to mobile phones (iTunes didn't even launch in Japan until June of 2005).

The impact of music subscription services is unclear. Then there are the subscription music companies like Real Networks' Rhapsody Unlimited and Yahoo's Music Unlimited. Steve Jobs has a funny quote about them: "I think you could make available the Second Coming in a subscription model and it might not be successful." I share some of his skepticism – to me, the idea of losing access to my music when I stop subscribing feels like blackmail. But on the other hand I know one of the senior guys in the music business at Real. He's wickedly smart, and I don't think he'd chase a useless idea. I haven't had a chance to do independent customer research on this subject, and it's possible that I'm just out of touch with how customers will behave, especially people younger than me.

The pricing structure for a music subscription service is completely different from a store like iTunes. To use Real's Rhapsody Unlimited for a year, you pay $120 and you can listen to all the music you want. If you want to keep listening to music, you have to pay again every year. Let's assume the case of a 20-year-old who lives until age 80. Over her lifetime, she'll pay $7,200 for music services.

That same investment in the iTunes music store would buy 7,272 singles, or one new song every three days for her entire life (for comparison, the average iTunes user today buys about three songs a month). For all but the most aggressive music users, a music subscription is a lot more expensive over your lifetime than buying songs – as long as you're thinking ahead 60 years. It's not clear that everyone does.

The situation gets more confusing when you look at the royalties for music used on subscription services. Believe it or not, no one knows what the royalties will be. The music industry and the subscription services have spent the last four years negotiating the issue, and they're still far apart. In the meantime, interim royalties are being paid into a holding fund; the musicians aren't being paid at all. The subscription companies want to pay 6.9% of their revenue in royalties, and the music companies want 14%. Even at that 14% figure, the lifetime royalty income from our 80-year-old-user would be only $1,008. The same user buying 7,272 singles on iTunes (even at just 99 cents a song) would produce royalties of about $4,700.

For music publishers and performers, selling songs is vastly more lucrative because they get a much bigger cut of the revenue. They have a strong incentive to see the subscription services fail.

No wonder the negotiations are so bitter. And no wonder Steve Jobs is so caustic toward the rental services – they get much higher margins than he does.

The negotiations may have to be decided by (brace yourself) the US Congress. There's no way to tell what Congress will do, and so there's no way today to tell if the subscription services will bring the tipping point closer or push it further away.

It's enough to make a person long for the "simple" days of vinyl records.

What will happen?

Anyone who tells you they know for sure what will happen to the music business is either delusional or selling something; the variables are too numerous and complex to make high-confidence predictions. But since I raised the subject here, I feel obligated to put a stake in the ground. So here's my guess:

Apple will eventually allow variable pricing on singles. That change has been slowed by New York state's investigation of the record companies for online song price-fixing. According to the LA Times, the focus of the investigation is on "most favored nation" clauses in which record company contracts mandated that they get the highest price for singles charged by any other record company. That would have the effect of jacking up prices automatically, the sort of thing the government frowns on. But the basic idea of a store charging more than 99 cents is apparently not at issue, and indeed some wireless music stores already do. So I believe that after holding out for another year or so to help solidify its dominance, Apple will eventually give in. The price of an online single will then settle at a balancing point that produces the most revenue without driving an explosion of piracy. I suspect (gut instinct here) that point is about $1.99 per song for current releases.

The move to variable pricing is essential to drive the economics of the tipping point, so I hope Apple will get on with it.

The tipping point will arrive in 2008 or 2009. Even if you can charge $2 a copy for an e-single, the financial case for an existing act to dump its record label and sell direct is difficult, because a current group needs to protect the revenue it gets from CD sales. But a newly-formed group doesn't have existing sales to protect, and it has the most to gain from the lower barriers to entry in online sales. I think the tipping point will come the first time a new music act, selling online, is able to make serious money from a hit single, without ever bothering to create an album, burn a CD, or sign with a record company. That example will incent a new generation of performers to bypass the record companies. Their critical mass of fresh talent will drive up e-music sales further, producing a self-reinforcing transition away from record industry control. Another gut guess: I think we'll hit the tipping point when you can sell a single on iTunes for $1.99, and when US e-music unit sales hit about a third of total music sales. If current growth continues (always a dangerous assumption), the tipping point could come in 2008. Call it 2009 if you want to be conservative.

When that day comes, I suspect that Steve Jobs will be there with a Mac-based music editing program that has a "publish" button in it. Press the button, and your song is automatically uploaded to iTunes.

Parts of the record industry that add value will survive indefinitely. Some people will continue to want CDs -- either for nostalgia or because, for the time being, CDs have higher sound quality. Even in the e-music space there will still be roles for business managers who discover new artists and help them market, producers who improve the quality of their music, and concert promoters.

The number of independent record stores will continue to decline. This has almost nothing to do with online music; it's being driven by competition from the mass retailers like Wal-Mart (the #1 US music chain in album sales), Target (#3), and Amazon (#4). They skim off the most popular titles and sell them for aggressive prices, gutting the margins of the record stores (the same thing is happening to independent toy stores). E-music will at most just accelerate this trend.

Can anyone stop the iPod?

No.

The time to stop it was two years ago. At this point the real question is whether anyone in the US can even keep up. The iPod is a system that includes both an online service and devices, and I think the only way to compete will be with full systems. Few companies with a presence in the US have both the skills and resources to do that. Microsoft can. Nokia can. Google and maybe Yahoo can. A stock analyst claimed in January that Google is planning a music store . Almost everyone in Silicon Valley would enjoy watching an Apple-Microsoft-Google cage match, but I think Google will be the first one hit in the head by a folding chair unless it also makes the devices.

Outside the US, the picture's much less clear. There aren't a lot of systems-oriented tech companies anywhere, but iTunes is much less established in many other countries, so there may still be time for smaller companies to make a play. In Japan, I would never bet against the two leading operators, NTT DoCoMo and KDDI.

The new powers in the industry will be the big online music stores. By featuring particular artists, they'll be able to make careers. Which e-music stores are likely to be dominant? In the US, Apple has a big lead in sales and an enormous lead in momentum. I dearly hope they won't be the single dominant store – if there's effective competition, it'll keep music prices low, give more of the rewards directly to artists, and make it easier for new acts to break into the industry. And that's the outcome that would make this whole complicated, painful transition worthwhile.

That's my take on things. What do you think? Do you have fixes to my analysis? Disagree with my conclusions? Please leave a comment – I'm interested in your perspective.

Next in Removing the Middleman: ebooks. And you thought music was complicated.

________________

*The music sales chart is based on figures from the RIAA (a music industry trade group), Rolling Stone, IFPI (another music industry trade group), and numbers extracted from a nifty historical chart prepared by Karl Hartig.

More info:

An organization called Future of Music Coalition has done a lot of analysis of music economics, from the perspective of an artist. I think it's very rational stuff, and a nice counterpoint to the strong rhetoric you hear from the tech companies on one side and the record companies on the other. I thought their analysis of iTunes was especially good. Highly recommended.

IFPI's report on global music downloads is interesting, even though it reads like it was written by a PR agency. It has some interesting tidbits on what's happening outside the US.

The Economist did a nice overview of the music industry.

There's a book and weblog called The Future of Music that talks about many of these issues. The authors have been in the music industry for years, and some of their conclusions are very different from mine. Check them out and you can make up your own mind. Also, I want to give them credit for pointing out the Rolling Stone quote that I used at the start of this post.

Removing the Middleman, Part 2: Music

LifeDrive: Palm's own eierlegende Wollmilchsau

The Germans have a great phrase: "egg-laying woolly milk pig." That's the term for a product that fails because it tries to be everything to everyone.

In a speech at a PalmSource developer conference several years ago, I described Pocket PC as an egg-laying woolly milk pig, and I think that's still a good explanation of why it's popular with enthusiasts but has failed to broadly expand the handheld market. Unfortunately, though, I think the strongest example of the syndrome on the market today may not be a Pocket PC at all. It's the Palm LifeDrive.

It is difficult to determine exactly how the LifeDrive is doing in the market, but there have been hints that sales haven't lived up to Palm's expectations. In September 2005, the company blamed a revenue shortfall in part on slow sales of the LifeDrive. I don't have access to NPD's US retail sales reports, so I can't directly check the LifeDrive's sales. I hope they have improved. But I suspect sales have continued to be less than stellar, or Palm would have bragged about them.

If sales are slow, that would be a shame. I think the idea of a hard drive in a handheld is great, because it enables some wonderful solutions. Although four gigs of storage doesn't sound like much in PC terms, it's an incredible slug of data if you manage it well. Even without compression, four gigs is enough to hold the text of more than 10,000 novels – one a day for 27 years. It can easily hold the text (although not attachments) of every e-mail message you will ever send or receive in your entire life. It can hold enormous reference databases, and huge collections of business documents. It can be, in short, an archive of all the meaningful documents in your life. It's ultimate brain extender, your own personal memory supplement that you can carry with you at all times.

For those of us in information-heavy jobs, a product like that would be ecstasy.

But for that archive to work properly, it has to be wedded to a wickedly fast search engine, and you need very clever software tools to scrape the right data from your PC and the Web. You don't want to be forced to load four gigs of information one document at a time, and the archive is useless if you have to use a traditional folder metaphor to travel through it.

Unfortunately, Palm didn't wrap that sort of comprehensive data solution around the LifeDrive when it was launched. Instead, the product is bundled with a little bit of software for managing documents, and a little bit of software for carrying media files. Instead of focusing on one particular solution and utterly nailing it (the way Palm did with the Palm Pilot and the Treo), Palm crammed two contradictory solutions into the LifeDrive and didn't deliver either one of them thoroughly. On the one hand LifeDrive is supposed to be a mega-entertainment device, capable of holding tons of songs and photos and other content. But it lacks a slick, fully-integrated content-acquisition system like the iTunes music store, and at $450 it's far too expensive for the young adults who want entertainment devices.

On the other hand, the LifeDrive comes with PC document compatibility software, but lacks comprehensive tools for automatically scraping all your key files, web pages, and e-mails into the device, and doesn't have the right sort of search capability to turn those files into a personal archive. What's worse, the media features of the LifeDrive are likely to alienate heavy data users. Information-centric people can afford to pay $450, but they're the most serious of users, and are generally resistant to anything that smacks of mobile entertainment. The fun and entertaining side of the LifeDrive chases those customers away.

If you want to see the scattered identity of the LifeDrive in action, you can start with Palm's own website. The home page for the LifeDrive declares that it's great "at the office, at the hospital, on campus, and on vacation." The usual test of a good product positioning is that in addition to telling you who the product is for, it should also tell you who the product is not for. If you haven't excluded some customers, you haven't been specific enough to please anyone. Treo, for instance, is a professional business product. It's not for students, and it's not for soccer moms. But as far as I can tell, the LifeDrive is for everyone over the age of eight who has $450 to burn.

Another symptom of an egg-laying woolly milk pig is that the manufacturer resorts to a lot of technical specs in order to sell it. Since the product is basically a bag of features, that fact seeps out in the product description. Here's the main text from the LifeDrive web page:

"For those who demand more, palmOne introduces the all new LifeDrive(tm) mobile manager. With a huge 4GB hard drive and built-in Wi-Fi(r) and Bluetooth(r) wireless support, you can easily carry all the essentials of your busy life and use them as you will. • office docs • Word, Excel and PowerPoint docs from your desktop computer, 300 songs, 2 hours of video, 1,000 vacation photos, and more, are always with you. • email & web • With support for POP, IMAP and Exchange email accounts, you can stay on top of your email at any of the thousands of Wi-Fi hotspots around the world • music, photos & video • Plus, a voice recorder, MP3 player, and photo viewer keep your precious few moments of free time both more interesting and productive."

Wow, you have only a few precious moments of free time, but we'll make them more interesting and more productive. Unfortunately, most people want one or the other.

There was a time when Palm prided itself on not drowning customers in technical specs. Part of the company's positioning was that true power came from what the product did, not what parts went into it. Thanks to the Internet Archive's magnificent Wayback Machine, here's Palm's online description of the Palm Pilot, from early 1998. Compare it to the LifeDrive text above, and note the absence of acronyms and numbers:

"The PalmPilot(tm) connected organizer is the ultimate personal and PC companion. With this easy-to-use, powerful handheld device, you can manage your schedule, personal information, contacts, and e-mail -- whether on the road or at your desktop. A PalmPilot organizer lets you fit a world of information into the palm of your hand. With a touch of the HotSyn(tm) button, everything you've entered into your PalmPilot organizer is synchronized with your desktop computer, and vice versa. It's not just a backup of information - it puts the most up-to-date information you need at your fingertips, wherever you are."

Some of the basic ideas are the same as the LifeDrive, but they're expressed with much less techno-speak. And the core use of the device is clear. You can decide pretty easily if you want this product. That's what happens when you focus your messaging properly.

I hope Palm won't give up on the LifeDrive. I think it can't be an iPod replacement because Palm doesn't have the right online services, and because the product's far too expensive. But if they cut out the cute stuff and beefed up the data capabilities, I think it might be an awesome product for businesspeople and academics who need to deal with huge amounts of information.

Which mobile device companies get it?

PDA 24/7 just ran an interview with me. In one of my answers, I talked about which device companies "get it" – which ones understand how to make a truly effective smart mobile solution. Looking back at my answer, I realized I had left out a couple of companies. I want to correct that oversight.

Before I list the companies, I should explain what I mean by "get it." I think that a truly effective smart mobile device must be both focused and integrated. By focused, I mean that it must first and foremost solve one particular problem for a particular type of user. Kitchen sink products that try to be everything for everyone sell to enthusiasts but no one else. The companies that get it specialize in leaving out features that aren't essential to the core product.

By integrated, I mean that the product must combine hardware and software (and in some cases wireless services) seamlessly to produce a product that just works. People usually tend to use mobile devices in short spurts while they are on the go. This makes them very intolerant of even small usability problems that might be overlooked on a PC. If the user must hassle with configuration, or if the user experience isn't dead simple, you're back to selling to the enthusiasts.

Most companies in the mobile market don't know to design like this, either because they don't know how to make hardware and software together, because they're not good at usability, or because they don't know how to focus on solving a single problem. The lack of these skills is holding back progress in the mobile market, so it's worthwhile to study the companies that know how to do it. Here are the ones on my list:

Nintendo: Differentiation, not features. Frequently written off by the feature-centric press, Nintendo has continued to succeed because it focuses on a particular market (gaming) and type of customer (young people), and it adds features that do special things for them. My favorite example is the Nintendo DS gaming device. A technophile would ask for WiFi, a high-res screen, and a faster processor. Instead Nintendo added a second screen – and a touchscreen at that. Nintendo then designed applications that take advantage of the touchscreen to create a unique gaming experience.

This is a classic example of designing for the solution. The traditional PC-style design approach says you have to be "up to date" in all of your specs in order to sell well. Nintendo realized that its customers don't care abut features as much as they care about the gaming experience. Nintendo doesn't add features, it adds differentiation.

I don't know if Nintendo will manage to survive forever in the face of the overwhelming financial muscle of Sony and Microsoft, but if it loses I think it'll be because it was spent into oblivion, not because it lost touch with its customers.

Apple: A solution, not a product. It's hard to remember today, but there was a time when MP3 players were viewed as a curious little niche, and many people were skeptical that they'd ever amount to a truly large category. Apple changed that.

The folks at Apple realized they weren't actually selling a music player, they were selling a music purchase and playback system. I think their integration of the whole thing, from iTunes out, is what made the iPod take off.

Apple has wisely resisted most of the advice to load new features into the iPod. Although video has been added, I think it's the exception that proves the rule. Apple could have opened up the OS to third party apps, added a touch screen, built in WiFi and Bluetooth, and an SD slot. Apple could, in short, have transformed the iPod into a Pocket PC. Smart move that they didn't.

In addition to creating a nice business for Apple, this systems focus creates huge barriers to competitive entry and commoditization. To match Apple's solution, a company needs to duplicate the iPod itself, the iTunes music store, and all of the business development deals that Apple has made with the music industry. It's not impossible for a competitor to replicate this, but it's enormously more difficult than copying a piece of hardware, and it takes a lot more investment. The hardware-cloning shops of Asia, looking at that huge mountain to climb, tend to focus their efforts elsewhere.

Apple's well aware that it gets it. Here's Steve Jobs in Rolling Stone magazine: "We do, I think, very good hardware design; we do very good industrial design; and we write very good system and application software. And we're really good at packaging that all together into a product. We're the only people left in the computer industry that do that. And we're really the only people in the consumer-electronics industry that go deep in software in consumer products."

Steve's exaggerating a little, but after all the times he's personally been written off by the industry, I think he's entitled to brag.

RIM Blackberry: Patience pays off. You've heard it before – the old folks who reminisce and say things like, "I remember ol' Georgie Bush when he was just a little so-and-so getting blitzed at frat parties." Well, I remember RIM when it was a weird little Canadian upstart making e-mail pagers. The company wasn't flashy. It didn't hold big parties like us important companies in Silicon Valley, its products couldn't be bought in consumer electronics stores, and oh by the way it ran on an obsolete paging network.

RIM's current success was many years in the making. It carefully built up a franchise in targeted corporate markets. Selling to those companies takes years of patient work, while they do trial deployments and make you prove yourself. RIM gradually got its servers into a huge number of companies, which resulted in an explosion of device sales once the trial deployments were finished. RIM also took the time to create a very reliable e-mail management network, something that is not at all easy to do. It integrated its products very nicely with Outlook, the leading corporate e-mail system. It carefully honed the user experience for mobile e-mail users. And for its first few years it rented time on a paging network that had excess capacity and was therefore inexpensive.

I'm not completely comfortable with everything RIM's done. The company was very aggressive at enforcing its patents against competitors, which set the stage for others to do the same thing to it. And it has been very slow to deliver on its promises to let its service run on other companies' devices. But to me, the most important lesson from RIM was its single-minded focus on doing e-mail right and building its market over time. It had a vision, and it methodically implemented that vision over a period of many years – far longer than most Silicon Valley companies would persist at anything.

Palm: Obsession with detail. I wasn't with Palm during the days when they first designed the Pilot, unfortunately. But I spent a lot of time with people who were there, and the thing about them that impressed me most was their passionate obsession with tiny details.

They could sweat pixel placement and interface flow better than any bunch of people I've met before or since. It wasn't a science they were practicing, it was a craft in which they went over and over and over the details of how a typical user would operate the product, constantly asking how they could save that user a half-second in time or a moment of confusion.

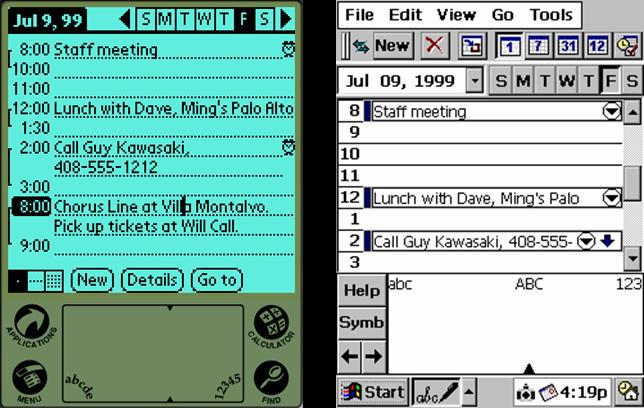

The interfaces they designed weren't always pretty. In fact, they were often darned ugly. But they were amazingly efficient in the way they used screen real estate. Here's one of my favorite examples:

This is Palm (left) and Pocket PC (right) circa 1999. I deliberately chose an old example because I don't want to get sidetracked into an argument about whose interface is better today.

Some important things to notice in these images:

--The Pocket PC screen has about 40 clickable icons and controls, the Palm one about 24. More isn't better in this case, because the Pocket PC screen is bewilderingly complex.

--It's hard to see from a static screen, but the Palm calendar lets you tap in an entry and edit it directly (you can see the text cursor in the word "villa"). On Pocket PC, tapping in an appointment opens up a separate dialog box to edit the item. That's a waste of time.

--Although the Palm screen has a smaller active area, you can read more of the calendar than you can on Pocket PC. That's because Palm blanks out unused hours, whereas Pocket PC tries to replicate the look of Outlook, where every hour is displayed. That works much better on a PC than it does on a tiny handheld screen.

Those little touches like editing in place and hiding unused hours didn't just happen, they were the result of many hours of agonizing effort by the designers at Palm.

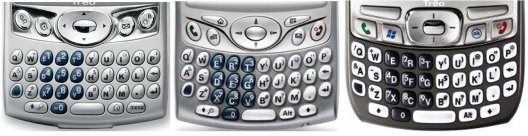

A more recent example -- look how the Treo keyboard has evolved:

From left to right, these are the Treo 600, the Treo 650, and the Treo 700. Look carefully, and you can see how the designers at Palm are thinking. In each product generation, they've rounded the corners of the case a little more. This makes the device look and feel thinner. They've added more of a "smile" to the keyboard (which makes it easier to round the edges), and they've steadily increased the color contrast between the keys and background. The buttons themselves have become more square, which gives more room to print letters and icons on them. Squaring the keys also makes them larger, which may make it easier to press them with a thumb (although I worry that it also has the effect of making the keys closer together). Overall, Palm is gradually figuring out how to make the best use of every millimeter available to them.

This sort of incremental, obsessive rethinking is typical of Palm's best designers. Nothing's ever perfect.

Although Palm spends a lot of time on hardware and user interface, the thing Palm hasn't tried lately is creating an online or wireless service to go along with its devices. Palm dabbled in that once with its Palm.net service for the Palm VII, and it worked very nicely. Unfortunately the company didn't build on it. It will be interesting to see if a future Palm solution includes an online component.

Danger: Lots of potential. I think Danger deserves honorable mention here. They haven't been as successful as the other companies I listed, but I admire their focus on making a communicator for the youth market. Even though they're stuck with the weakest major US carrier, they've produced pretty good sales – in the monthly unit numbers I used to get, the Danger device often outsold any single model of RIM Blackberry at TMobile.

This level of success has been achieved even though the Danger device lacks an MP3 playback capability, something that's almost essential for the youth market. If Apple really wanted to create a great music phone, they ought to build iPod capability into a Danger device.

There you are, my four (and a half) companies that "get" the smart mobile market. What do you think? Does anyone else belong on the list?

Removing the Middleman, part 1

"The first thing we do, let's kill all the carriers."

--Henry VI Part 2, as performed by the Silicon Valley Royal Shakespeare Company

I want to let you in on a little secret: the company most disliked by people in Silicon Valley is not Microsoft. It's not Google either. And no, it's not Intel, Apple, eBay, or even SCO.

Don't get me wrong, there are plenty of people who want those companies dead, but even the hostility toward Microsoft at the peak of its power pales in comparison to the contempt that people in Silicon Valley reserve for the companies that own the pipes: the carriers, networks, publishers, and content distributors who deliver entertainment and communication to consumers.

Most of the nastiness is expressed in private conversations in hallways and restaurants, but occasionally a bit of it boils over into public view...

"Carriers haven't been hot-houses of innovation, they've been charnel houses."

--Nathan Torkington of O'Reilly Radar

"The post-millenium world’s biggest adversity is the monopolistic control over the broadband pipes in many countries including United States."

--Om Malik of Business 2.0

(Silly me, I thought it was terrorism or maybe global warming.)

"It's amazing how the labels always seem to come up with new ways of screwing artists: if they're not cheating them out of royalties, they're systematically alienating their fan-base."

--Author and commentator Cory Doctorow

"Apple's never been very good at going through corporate orifices in order to get at the end users. And if we can't do it with 500 companies, you can imagine it's even harder when there are only four."

--Steve Jobs, on selling products through the US operators.

(Everyone in Silicon Valley knew which orifice he meant.)

Why's there so much "negative energy?" There are cultural disconnects and lingering bitterness over business deals that went bad during the bubble years, but the main issue is that the pipe companies are just plain in the way of what Silicon Valley wants to do.

For example:

No recording of digital radio. The music industry is lobbying for legislation that, if I understand it correctly, would:

--Prohibit recording digital radio broadcasts (satellite or terrestrial) in less than half-hour chunks.

--Prohibit recording digital radio based on any user preferences, including artists, genres, and song titles.

--Prohibit disaggregation of the recordings (ie, cutting out the commercials).

--Prohibit any recording at all onto any removable media or digital outputs.

Basically, it not only prohibits any TiVo style services for digital radio, it also bans almost any practical recording of digital radio.

High pricing and limited availability of eBooks. Ebooks are much cheaper to produce than printed books. An ebook doesn't have to be printed, distributed, stored on a shelf, or returned if it doesn't sell. Despite these savings, and their potential to make books available to more people, the publishing industry doesn't make many best-sellers available as e-books until they have been on the market for a while. For example, I just checked the NY Times hardcover bestseller list, and I couldn't find any of them on eReader.com, which claims to be the world's biggest ebook store.

Even when books are made available, most of the publishing industry insists that ebooks have to be sold for virtually the same price as printed books, even though they are massively cheaper to produce. Check out these books that were featured on the home page of eReader:

SuperFoods HealthStyle

Print price: $16.47 on Amazon

ebook price: $17.96 on eReader

Star Wars: Dark Nest, Book 2

Print price: $6.99 on Amazon

ebook price: $6.64 on eReader

The Five Lessons a Millionaire Taught Me

Print price: $10.17 on Amazon

eBook price: $8.54 on eReader

As far as I can determine, the publishers' main motivation for doing all of this is to protect the current book sales channels. The publishers are also afraid of ebook piracy. I think most of them would be happier if the whole ebook concept just went away.

That's good news for the Barnes & Nobles of the world, but it cripples the adoption of ebooks. Consumers want to read what's popular now, and they rightly ask why they should pay the same price for a digital copy as they pay for a tangible object. In 1999 I worked for SoftBook Press, an e-book company. This issue helped to drive them out of business.

Mobile phone companies: paternalism and slow innovation. The mobile phone industry is notorious for trying to create "walled gardens," tightly controlled collections of content and services for which they charge substantial fees. They tend to put obstacles in the way of open, unlimited access to the Internet, and are much slower to enable new services than Web companies are. I've had some mobile software developers tell me they were forced out of business because their funding ran out before the operators gave them permission to operate.

There are sometimes good reasons for the operators' caution – they've been burned by a lot of failed data services (can you say WAP?), and they're afraid rogue software might somehow attack and destroy their networks. But the feeling among many tech companies is that the operators are using this as an excuse rather than actually trying to solve the problems. They believe the security fears are just a smokescreen for trying to extract more money from users and software companies. After all, the world's ISPs have managed to live with open access over phone lines and cable networks for years, and nobody's network has been destroyed.

The operators are also seen as paternalistic toward users. I have vivid memories of a meeting with a major US operator in which we discussed the fact that a very popular phone in Europe had low sales in the US. I cited that as an example of how different the markets are around the world. "Oh, no, I can explain that," the operator replied. "We don't like that company and we won't let them sell their phones here."

That attitude, in which the operator does the thinking for the customer, is incredibly uncomfortable to most Silicon Valley companies. They are used to selling directly to end users, and don't want to work through anyone else (thus Steve Jobs' comment about "orifices"). They want the operators to be neutral providers of all products and services, enabling customers to make their own product decisions. That's the way the wired Internet works, and Silicon Valley wants the same thing in wireless.

Differential pricing on broadband. BellSouth and a number of other ISPs are starting to talk about charging websites for priority delivery of high-speed data. Aside from all the hostility this is generating among users who already paid for high-speed service, such a fee on high-speed delivery is seen as a barrier to small companies creating new data-heavy services. Such companies are often the most innovative, so this could have a chilling effect on Web innovation. As US chief justice John Marshall put it, "the power to tax involves the ability to destroy."

Those are just a few of many, many, many examples. Taken together, they are creating an almost endless appetite in Silicon Valley for business plans that feature the destruction of carriers and content publishers, even if the plans are longshots. For example, I think a lot of the enthusiasm around here for WiFi and VOIP is driven by a visceral hope that someone will find a way to use them to bring down the phone and cable companies.

From what I hear, most of the pipe companies hate and fear Silicon Valley right back. Here's a nice article from the LA Times on Hollywood's paranoia about Google.

I'm not trying to say either side is inherently evil. The industries just have different histories, perspectives, and interests. They don't see the world the same way, and they want different things. It's fair to ask if they might be able to learn to cooperate over time. Can't we reason together? Can't we find a common ground? Can't we all just get along?

Nah.

This isn't just a misunderstanding, it's a collision of market forces. It's going to be a fight to the death, or at least a fight to the severe disabling head wound. No amount of diplomacy can change that. Besides, I think it would be wrong to try. If we simplify the pipes in the right way, I think it would be a big benefit for consumers, for content creators, and for the economy as a whole.

The problem (and the opportunity)

Over the years, a series of elaborate, multi-step business mechanisms have evolved in order to move entertainment and communication from creators to consumers. (Books, for example, go from authors to agents to publishing houses to printers to bookstores to readers.) Those systems all have three things in common. First, in most cases, the vast majority of the money paid by the consumer is absorbed by middlemen rather than the content creators. Second, the middlemen view their points of control as entitlements, and will fight like rabid wolverines to keep them.

And third, the Internet and new technologies create potential mechanisms to break their control, radically simplify the distribution chain, and enable a much higher percentage of the total revenue to flow back to content creators.

Today there's intense interest in some of the benefits we could get from new distribution channels. For example, the Long Tail weblog is focused on how new forms of distribution can make it economically viable to create content for narrow vertical markets (the "long tail" at the end of the demand curve).

But many of the ideas aren't new. The late Peter Drucker once predicted that electronic publishing was on the verge of making magazines obsolete.* Today, 28 years after he made that prediction, electronic publishing is still on the verge of making magazines obsolete. This is typical of much of the analysis of new content channels – it tends to focus on the benefits and gloss over the process of getting from here to there. We assume the benefits are so compelling that it'll just happen. But in my experience the real world doesn't usually work that way. If you dig into the details, there's usually a tipping point that combines economic models, new technology, and new business infrastructure that must be created before a new channel takes off. If any element is missing, the transition never happens at all.

The barriers are very different in each industry, which means the pipes won't all change at once, and some of them may not change at all. To figure out what needs to be done, you have to look at each case individually.

That's what I plan to do over the next few weeks. The first one I'm going to cover is music.

(Sorry to leave you hanging, but if I try to write this thing all at once I won't post anything until March.)

__________

*Adventures of a Bystander, Peter Drucker, 1978. If you don't already have this book, you should get it. Then check out the chapter on Henry Luce.

Is browsing the mobile data killer app?

Today we have a great case study in how incomplete statistics can confuse people about the use of data services on mobile phones.

A Nokia manager recently gave a talk on the use of data services on mobiles. The presentation said that 63% of packet traffic generated by smartphones is Web browsing. Unfortunately, the presentation is no longer posted, but it was excerpted by Simon Judge's weblog, and subsequently reposted by Russell Beattie of Yahoo, who runs a very high-traffic mobile weblog that's a great info resource. Russell headlined his post, "Browsing: The Mobile Data Killer App."

When I looked at the source data, I couldn't find evidence to support that conclusion. I am not trying to pick on Russell here – the problem is not with his post, but with the incomplete data from Nokia. I'm hoping that when I can finally see the full presentation it'll have better documentation, but the pieces I've found so far are not encouraging.

If you've used a Nokia Series 60 smartphone, you'll know that they're not really all that smart. Most of them are not good e-mail clients because they don't have keyboards, and it's hard to find a lot of third party apps. Browsing is one of the most usable data features in the phones, so I'm not surprised that it's generating most of the data traffic. In the few slides I saw, Nokia didn't tell us the total amount of data traffic generated by the phones, so it's possible that browsing is generating 63% of a very small number.

That possibility is supported by another curious statistic on the slide – only 60% of the users have sent even one MMS (photo) message, and the people who do use MMS send an average of only 1-2 MMS messages per month. That means the average Series 60 phone is generating at best about one MMS message per month. When the carriers subsidized those camera phones to the tune of one or two hundred dollars each, it was with the expectation that they would produce a heck of a lot more MMS traffic than that. At that rate, the subsidy will never pay for itself, and the operators of the world have basically given free electronic cameras to several hundred million people and made no net profit from the exercise.

Simon's weblog also referenced a press release from Telephia, a mobile phone research company, that seems to have some similar statistical fuzziness. It says a survey shows much more aggressive mobile data usage by 3G users compared to non-3G users. For example, it says 56% of the 3G users browse, compared to 39% of non-3G users. 35% download video clips, compared to 11% of non-3G users. And so on. Unfortunately, what the press release doesn't say is what those 3G users did with their phones before they upgraded to 3G. Did 3G cause people to use more data, or did the heaviest users of data migrate to 3G? Without a before and after look at the billing history of the people who switched to 3G, we can't tell.

It's possible that Telephia did track the data usage of individuals, but the press release doesn't say so, and I doubt they did it because running a study like that is wickedly expensive. Without more specific information, we can't tell if 3G is actually increasing traffic and billing, or just giving a new (and heavily subsidized) toy to people who were already using a lot of mobile data.

Again, my point here is not that Simon and Russell are wrong, it's just that you have to ask a lot of probing questions about any industry statistics – especially those that claim to have discovered a killer app.

I'll take that bet

Scott McNealy as quoted by the Register:

"I guarantee you it will be hard to sell an iPod five or seven years from now when every cell phone can access your entire music library wherever you are."

Scott, I guarantee you that even if it's easy for any phone to access your online music library five years from now, most users will prefer to store the music locally so they don't have to pay a big wireless download fee every time they want to listen to Bohemian Rhapsody, and so the song won't stop in the middle when they go out of coverage.

Google Video: Is that all there is?

Google's new video store seems to be up and running. I say "seems to be" because when I looked at it my first reaction was, "Is that it? You guys used a CES keynote to announce that?" The interface is simple, as you'd expect from Google, but in this case simple means simplistic and primitive. The home page features three types of video – for sale, most popular, and random. To examine for-sale videos by category, you use a drop-down menu that lists each series available: classics like MacGyver, Star Trek Deep Space Nine, and Survivor Guatemala. This interface isn't going to scale to handle more than 20 or 30 series, and even now it does almost nothing to invite browsing or easy exploration.

The press has been saying that Google Video sets up a direct confrontation between Google and Apple's iTunes. If this is the best Google can do, iTunes is going to win in a walkover.

I have to assume Google is working on a better interface, but the fact that they made such a prominent launch event for something so disappointing implies to me that their marketing judgment isn't very good these days.

Despite all of that, I think Google Video is incredibly important. Not because it puts Google in the video business (I don't think all that many people will pay to watch videos on their PCs), but because of the infrastructure behind it. Google now has a billing engine.

I haven't been able to find all the details on how Google's billing works, but so far it looks fairly well thought-through. You can read a couple of articles here and here. The owner gets 70% of the revenue, and Google keeps 30%. That's a bit high; I think the right cut is 20%. The minimum price for a video is five cents, which really impressed me. The credit card companies don't like to process charges that small, so I don't know how Google's doing it, but it's a very good thing because it encourages impulse buying. It looks like we're finally going to get an Internet micropayment system with critical mass!

Google also reserves the right to take a bigger cut of your revenue if you consume an unusual amount of resources (I presume that means if your video is so popular that Google has to buy a new server to host it). The exact circumstances in which Google will take more are not spelled out, which makes me deeply uncomfortable.

Questions aside, the terms are a lot better than what mobile software companies get from online stores like PalmGear and Handango, which can keep 50% or more of your revenue. And that's my point. Now that Google has a billing mechanism, it can apply it to any form of electronic content – software, photos, e-books, music, articles, analyst reports, and so on. I think you could eventually see purchasing built right into search results – along with the option to translate a web page, you could have the option to buy a piece of content.

The next logical step is for Google to tie the billing engine to Google Base, so people can sell any electronic file through Google. This is potentially very powerful. Think of a small software developer looking to sell an application. Today they need to either sell through an online store (which takes a huge cut) or set up their own e-commerce site (which is a big pain in the neck). It's going to be enormously tempting to just offer your stuff through Google instead.

The Google vs. Apple video competition will be interesting, but ultimately I think video's a sideshow. Google's gradually setting itself up to be the middleman for anything that can be shipped electronically. I think that's the real importance of the Google Video announcement.

Thanks for the award!

I'd like to thank the folks at PDA 24-7 for naming Mobile Opportunity one of the two best mobile-related weblogs of 2005.

This would probably be a good time to say what I'm hoping to accomplish with this blog. I set it up as a way to share what I've learned about mobile computing, plus any other interesting tech-related information I run into in the course of my consulting work. So you're going to get a mix of mobile and non-mobile information. I'm not trying to advocate any particular company or product; I just want to help grow the industry and help users make well-informed decisions.

I'm trying for quality rather than quantity. I expect to post one or two times a week on average. Blogger produces an RSS feed, and I think that's a great way to read the material since I'm not posting every day.

I have received one report of a validation problem with my feed. I use Bloglines, and I know the feed works fine there. But if you run into problems, please contact me via the address here. Also please let know if you have questions or want to suggest any topics for me to cover.

Thanks for visiting.

Does the mobile OS matter?

Yes and no.

But mostly no. It doesn't matter the way the OS companies want it to.

Recently two telecom analysts in Europe published essays saying that there isn't going to be a winner in the mobile OS wars. The UK research firm ARC Chart wrote, "far from the market consolidating around one or two of major OS platforms, the number of middleware systems for which applications can be developed for is actually increasing.... The mobile OS story is no longer simply about a war between Microsoft and Nokia."

(Actually, the story was never simply between Microsoft and Nokia, even if you're watching only the European market. But that doesn't invalidate their main point.)

Then analyst Dean Bubley chimed in: "Let's face it, heterogeneity in mobile phone OS is permanent. At the bare minimum, Nokia will continue to champion Symbian, Motorola will push Linux, HTC is making a good living with Windows Mobile, and assorted proprietary OS's continue to make traction because consumers don't care.... OS diversity is a baseline. Most manufacturers recognise this, and most mobile operators as well."

Unfortunately, ARC Chart went on to theorize that middleware software platforms are going to take on the standard-setting role that the OS was supposed to play. They cite products like Brew, Savaje, and Action Engine as examples.

I don't think so, not if they behave the way the mobile OS vendors have behaved. I think the most important words were Dean's: consumers don't care. I wouldn't make the statement so categorically, but I think it is true that most customers don't care. Here's why.

The PC fallacy

As I mentioned in my post on the Myth of the Smartphone Market, one of the most common mistakes made by people in the mobile industry is assuming that their market will work like the PC market does. More often than not, it doesn't. If you use PC assumptions and PC reflexes to run a mobile company, chances are you'll lose your shirt.

This is why people who've worked a long time in the few really successful mobile data companies, like RIM and Palm, sometimes come off as smug and dismissive when they get advice from outsiders. If you approach them from a PC perspective, they'll tune you out faster than I tune out country music when I run into it on the radio.

One of the most basic assumptions of the PC world is that one OS eventually wins. Even if two operating systems start out even, one of them eventually gets a little better sales. Seeing a better chance of selling applications on that platform, more developers concentrate on it. The higher number of apps brings in more customers, who draw more developers, who attract even more customers. The process feeds off itself, and pretty soon one OS has 90% of the market and the other is called Macintosh.

For years almost everyone (including me) assumed the same effect would operate in mobile devices. But does it? Let's look at the evidence.

At the end of the century, the Palm OS took a commanding lead in mobile application development. The company's developer base grew from about 3,000 registered developers in 1998 to 23,000 in 1999 to 130,000 in 2000. The application base grew at the same rate, vastly outstripping everything else on the market. By all the rules of the PC market, this should have been the end of the game. As licensing increased the base of Palm OS devices, every other mobile platform should have been wiped out of existence.

But it didn't happen.

There are a lot of reasons why. Microsoft and Nokia were both willing to endlessly subsidize competing platforms, for example. But another key factor was that the "network effect," the bandwagon process in which a leading platform sucks up all the customers, simply didn't work. The users didn't behave the way they were supposed to.

It's the solution, stupid

What are the two most successful smart mobile devices on the market today? iPod and RIM Blackberry. What operating systems do they run?

Uh, well...

Last I heard, the iPod runs a mashup of software from Portal Player and Pixo. RIM runs its own embedded OS (I don't know if it's proprietary or derived from an outside product), plus Java. Neither of them have fully mature software platforms with a large range of third party applications, and yet they outsell the products that do.

"Wait," someone might object. "Those products just sell the best because they work best. If someone had a really good product on an open operating system, it might sell the best." And that's exactly my point. In PCs, the industry-standard operating system can propel even inferior hardware designs to leading sales (ask any Mac owner). The PC OS generates demand. In mobile devices, the "solution" – the device's main functionality – is usually what generates demand. The mobile OS doesn't matter. Or a more accurate statement would be, something else matters a lot more.

This wouldn't be as much of a problem if the mobile device companies were good at creating mobile data solutions on their own. Then they'd pick the OS with the best plumbing and build a great product on top of it. The OS still wouldn't matter to most users (it would be equivalent to a no-name embedded RTOS, something like TTPCom's Ajar or OpenWave's client software), but at least you could count on it to be an element in the best mobile devices.

Symbian has tried to follow this route. It's owned by mobile phone companies, and they generally don't want it to have anything to do with creating end-user value – the phone companies, particularly Nokia, view that as their turf. The restrictions are so tight that Colly Myers, former head of Symbian, says the company shouldn't have even tried to create a user interface for its product.

But most mobile device companies, especially the big ones, are terrible at creating integrated hardware-software solutions. They're hardware companies, not software companies. The mobile operators are little better; they generally understand voice but not data. So you get a three-way traffic jam of OS vendor, hardware company, and operator (if the device is a phone), none of whom are in a position to architect the whole solution and make mobile data sing.

I do think there's hope for an application platform to establish itself as a standard in the mobile world, but it needs to be structured and managed differently from anything that's on the market today. I'll write about that later this month. In the meantime, the industry needs to understand that smart mobile devices today are basically appliances. Most people buy them to solve one major problem in their lives, and they'll favor the device that is the best solution to that particular problem. Blackberry is the best solution for mobile e-mail, so people buy it even though it sucks at almost every other function. iPod is the best solution for mobile music, so people buy it even though it can't do much of anything else.

There are a relatively small number of users, like me, who care so much about having a multifunction mobile device that we'll pay more and compromise on other features (such as weight and simplicity) to get it. The Palm OS ones are very loyal to Palm OS, and the Windows Mobile ones are very loyal to Windows Mobile. Although we're very noisy on the web, we're actually a relatively small percentage of the population. There aren't enough of us to create the sort of mass horizontal market the consumer electronics and phone companies are looking for.

Does that mean mobile operating systems are dead? Nah, but if the OS companies want to have a major impact on the market, they need to step up to providing full solutions to major user problems, rather than just plumbing. Picture a version of Windows Mobile that includes a well integrated system for downloading and playing music. Or a version of Palm OS that comes bundled with a great corporate e-mail solution and software to handle attachments. Those mobile software products could sell well. What's dead (or at least uninteresting and low value) is mobile operating systems that try to succeed by just being great infrastructure. That worked in PCs, but it won't work in mobility.